Monetary Policy and Aggregate Demand

Week 05

March 9, 2026

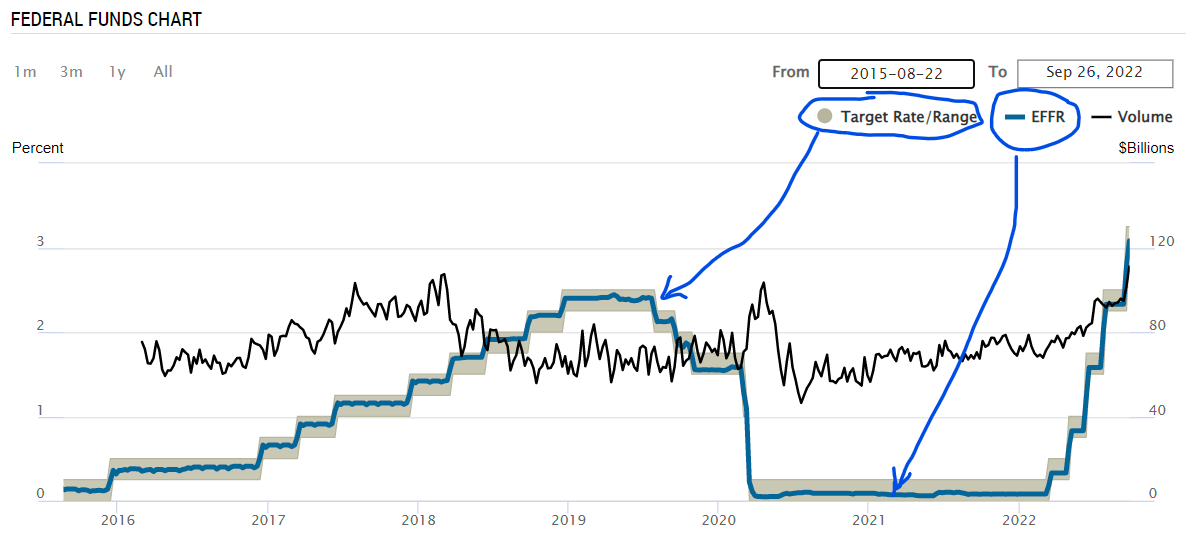

The Fed and the FFR

- A single image obtained from Fed New York shows all in a simple way:

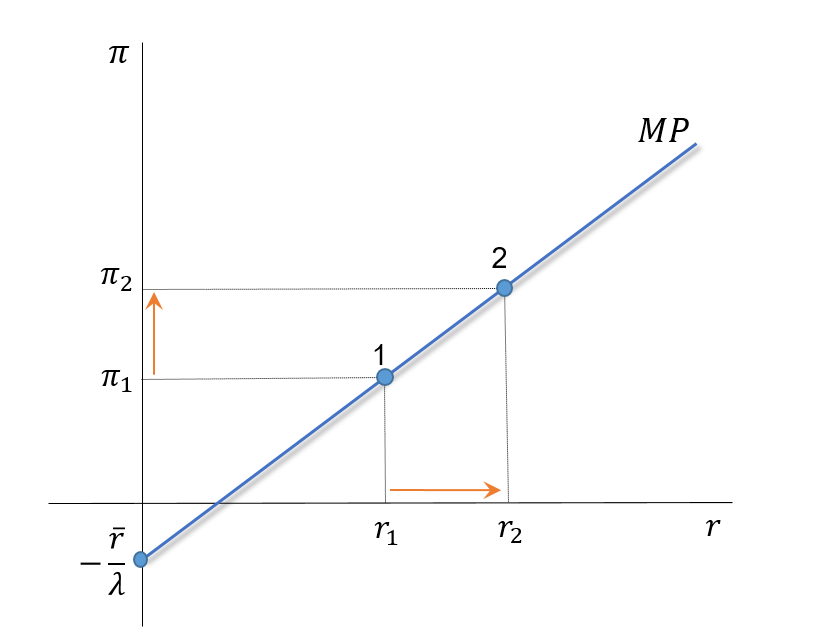

The MP Curve: Graphical Representation

The MP curve is given by: \(\quad r=\overline{r}+\lambda \pi\)

From point 1 to 2:

- As inflation raises from \(\pi_1\) to \(\pi_2\)

- The Fed is forced to increase real interest rates from \(r_1\) to \(r_2\).

- \(\Delta \overline{r}=0\)

- If \(\Delta \overline{r} \neq 0\), the curve shifts

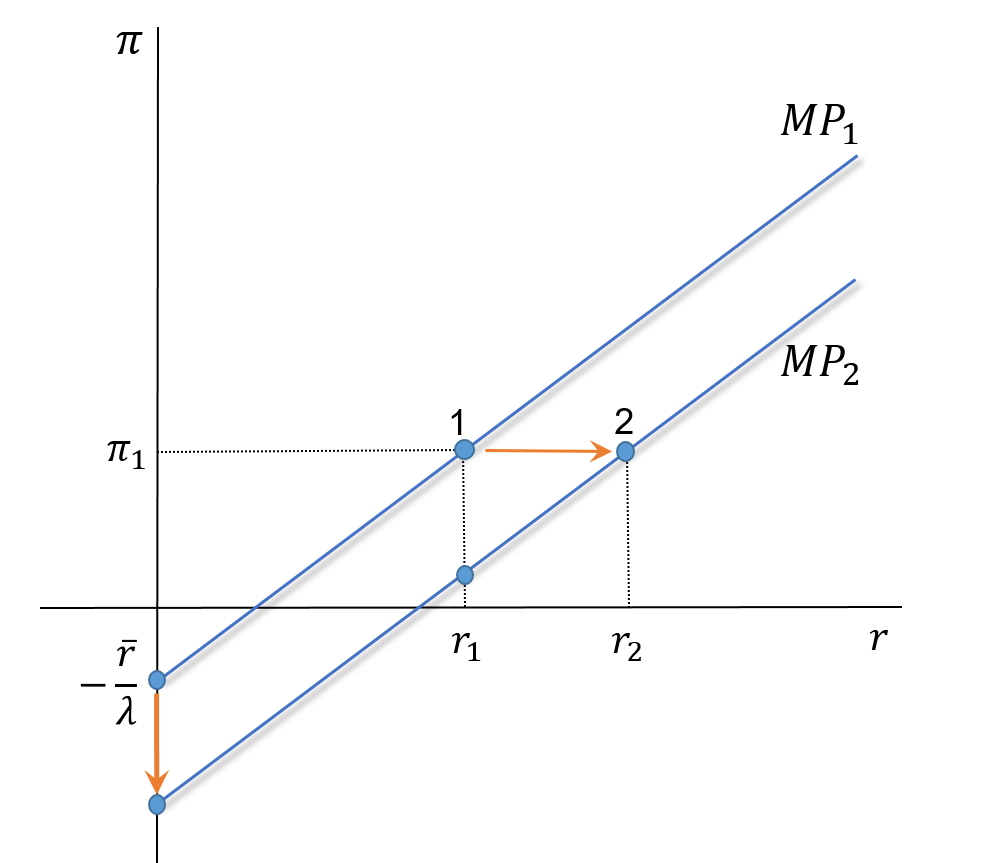

MP Curve: Shifts

The MP curve is given by: \(\quad r=\overline{r}+\lambda \pi\)

From point 1 to 2:

- If \(\bar{r}\) increases, the MP curve shifts to the right, and vice-versa.

- Notice that \(r\) increases, but \(\pi\) remains constant.

Policy and Practice

There are two types of reaction by the central bank:

- An accommodating monetary policy (movement along the MP curve)

- An aggressive monetary policy (a shift in the MP curve)

- In the figure below, can we distinguish between those two reactions?

![]()

Policy and Practice

- Two types of reactions? Why one? Why the other?

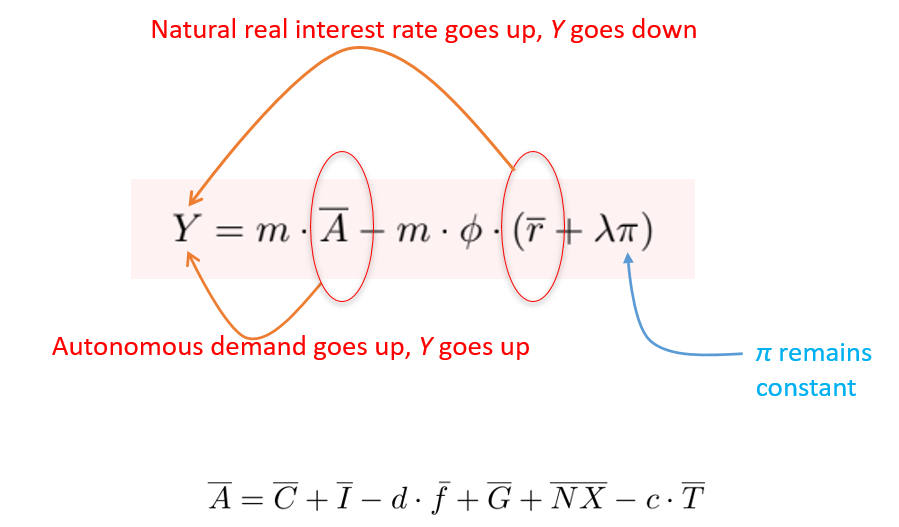

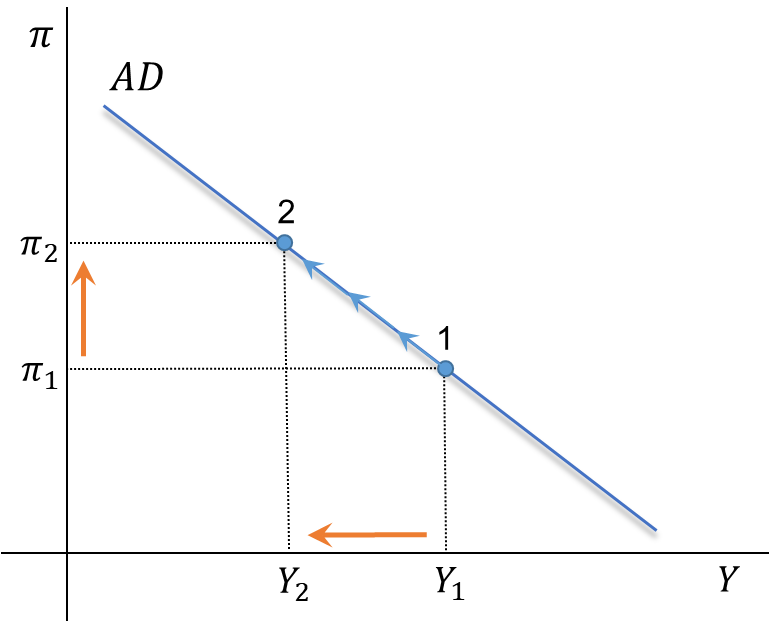

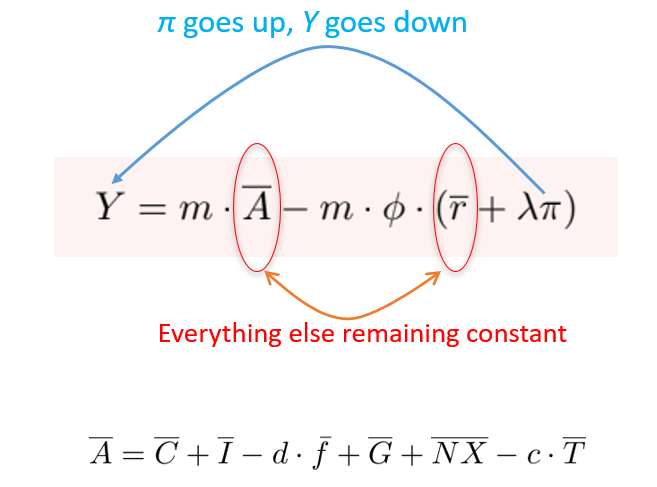

AD Curve: Graphical Representation

The AD curve is given by: \(\quad Y=m \cdot \bar{A}-m \cdot \phi \cdot(\bar{r}+\lambda \pi)\)

From point 1 to 2:

- If \(\pi\) increases, the central bank will raise \(i\) and \(r\)

- As \(i\) and \(r\) go up, demand will go down, and GDP will follow.

- This occurs if \(\Delta \overline{A}=0\)

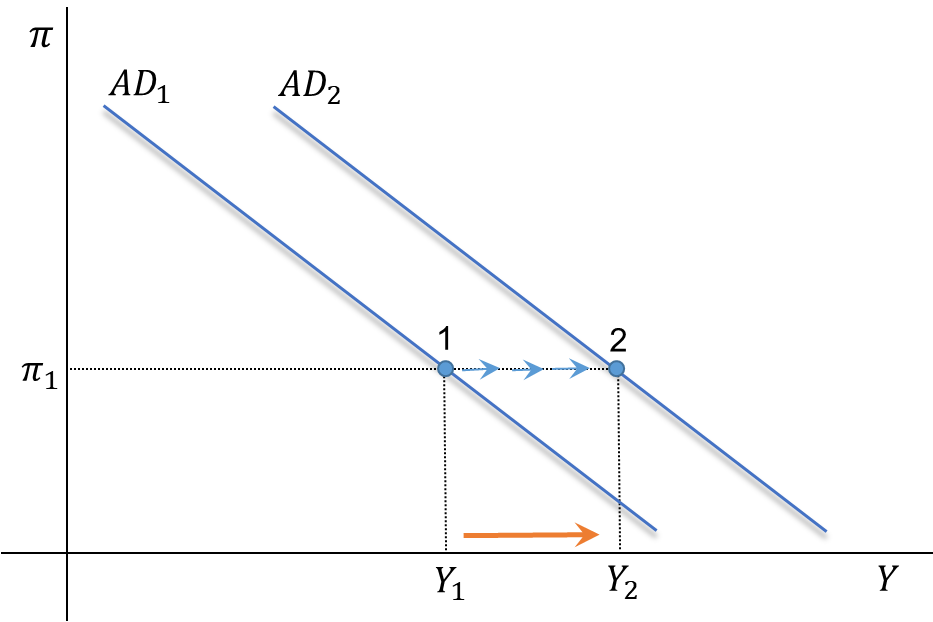

AD Curve: A Shift

The AD curve is given by: \(\quad Y=m \cdot \bar{A}-m \cdot \phi \cdot(\bar{r}+\lambda \pi)\)

From point 1 to 2:

- If \(\pi\) remains constant, the central bank will keep \(i\) and \(r\) constant.

- If those rates are constant, and \(\Delta \overline{A}>0\), then demand and GDP go up.

A Movement Along the AD Curve

A Shift of the AD Curve